As 2024 draws to a close, it’s worth revisiting the Portal Wars in the U.S. – and how little has changed. (View Highlight)

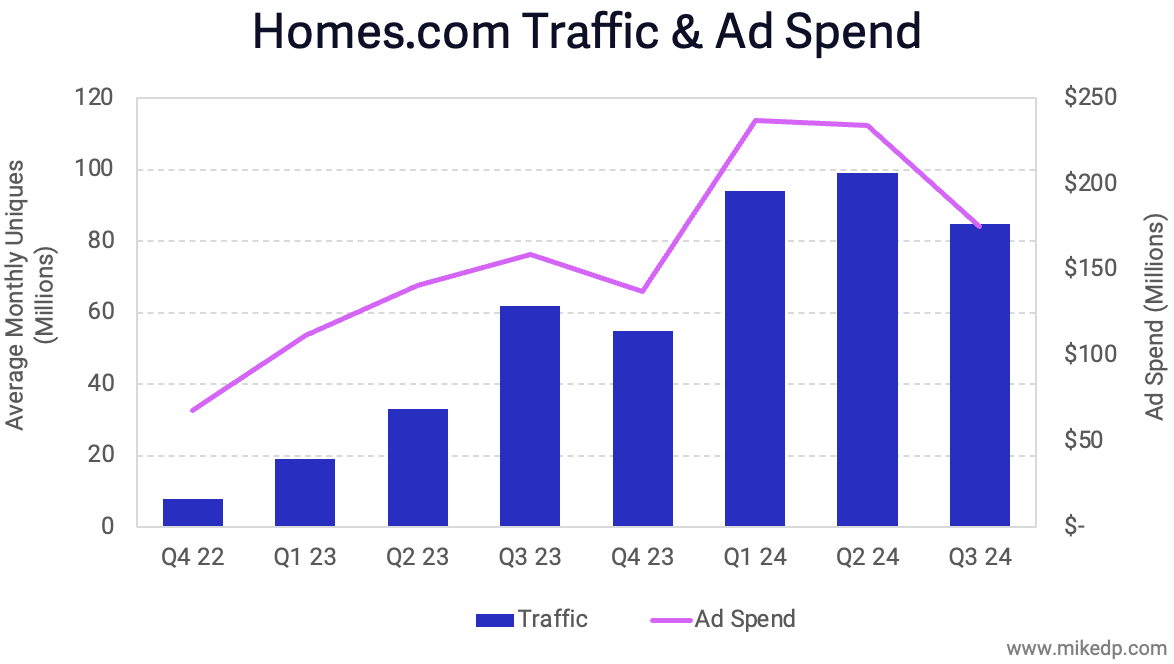

• The potential disruptor is CoStar, which has invested over $1 billion in Homes.com to challenge the incumbent portals for dominance, with traffic growing alongside a massive advertising spend.

(View Highlight)

Corresponding revenue growth has slowed and pales in comparison to the established portals.

• In the latest quarter, Zillow’s real estate lead gen revenue was about 20 times higher than Homes.com’s.

(View Highlight)

Zillow’s lead over the #2 portal realtor.com, as measured by real estate lead gen revenue, has remained relatively constant over time – and if anything, has increased.

• The recent uptick could be a result of strength in a down market, Zillow flexing its Flex muscle, or just slower growth at realtor.com.

• But the result is key: the #1 portal’s competitive position tends to get stronger over time.

(View Highlight)

The same scenario has played out in Australia and the U.K., where the leading portals command a significant revenue lead over their rivals.

• Interestingly, that lead is similar in all three markets – an average of 3.3x and increasing over time.

• The #1 portals stay strong and get stronger over time, the beneficiary of network effects, with no examples of that dominant position being eroded.

(View Highlight)

The bottom line: Real estate portal competition is like chess without checkmate; there’s no winning move, and it’s not a game that can be won.

• There’s a flurry of activity, tactical moves, and strategic plans, but very little actually changes; traffic may increase in a non-zero sum manner, but revenue – the ultimate metric of delivering value to paying customers – remains competitively static.

• Portal competition is exciting, but it’s unlikely to materially change the landscape – which is a perfect example of the DelPrete Probability Paradox in action. (View Highlight)

As 2024 draws to a close, it’s worth revisiting the Portal Wars in the U.S. – and how little has changed. (View Highlight)

As 2024 draws to a close, it’s worth revisiting the Portal Wars in the U.S. – and how little has changed. (View Highlight) (View Highlight)

(View Highlight) (View Highlight)

(View Highlight) (View Highlight)

(View Highlight) (View Highlight)

(View Highlight)